Share via:

How condo management services market monopolization could influence condo services market,

condo expenses and market values?

In the world of high-rise living, a seismic shift is needed to disrupt the current monopolistic tide that’s sweeping the condominium management sector in Toronto & GTA. The prevailing market landscape, defined by the unequal distribution of power among property management companies, casts a long shadow over the vibrancy of condo living. This article peels back the layers of this complex issue, using the latest market share data to shed light on the invisible chains nobody talks about but that could be driving up service costs and stifling innovation in condo service industries.

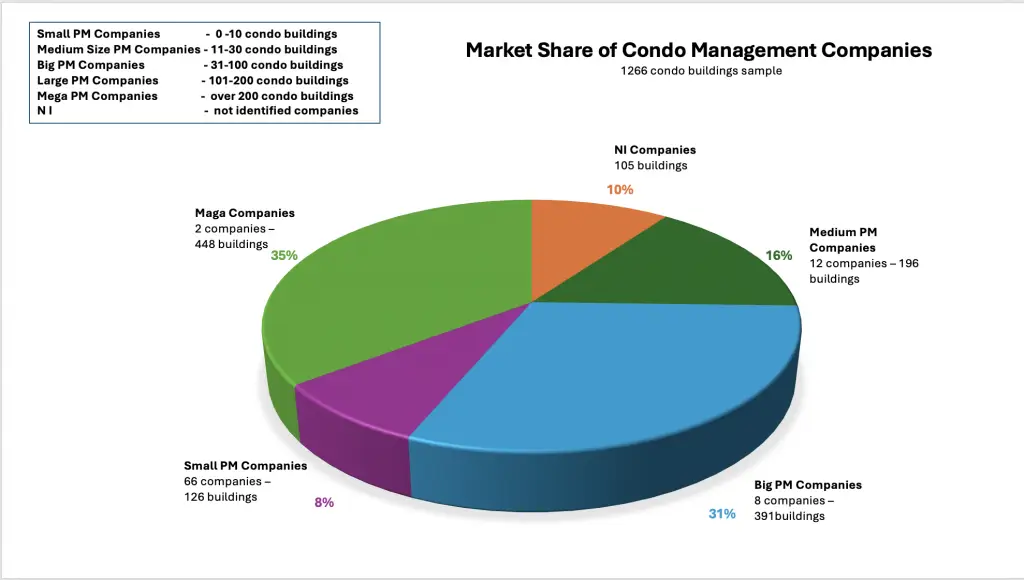

At the core of the conundrum is the heavy hand of Mega Companies, which, despite their minority (just two), manage a disproportionate about 35% of the buildings , creating an environment ripe for monopolistic tendencies. The evidence points to just two mega entities controlling 448 buildings (of those 1266 buildings that are ~ 50% all buildings in Toronto) , their vast reach potentially enabling them to command higher service fees, a cost ultimately borne by condo owners. The shadow of these giants looms large, threatening to obscure the competitive sun that could foster fair pricing and innovative service offerings.

Yet, it is not just the “Goliaths” that define this market, Medium and Big-sized condo management companies, with their 47% combined share, hold the keys to either bolstering the mega trend or breaking the mold to encourage competitive pricing strategies. Their decision to either align with the giants or champion competitive practices could tilt the scales in favor of the consumer or the corporation.

The small property management companies, with their 8% hold, seem like mere spectators in this game of thrones, their limited influence reflected in the fragmented nature of their market share. They stand as a testament to the multitude of potential that is yet to be tapped, offering hope for a more diversified and competitive future, if only the barriers to entry could be dismantled.

Amidst this complex network, an enigmatic 10% of the condo buildings in this sample is managed by unidentified companies or managed by condo boards. This group of building indicated the highest financial efficiency of condo expenses (as market value per square foot divided by annual condo fee per square foot), and it becomes a breeding ground for a fair competition.

The market share illustrated in the pie chart reflects the distribution of condo buildings among property management companies of varying sizes. Here’s how such a market share distribution might influence condo owners’ service prices:

- Dominance of Mega Companies: The chart shows that ‘Maga Companies’ (presumably a typo for Mega Companies) control 35% of the sample of buildings with only 2 companies managing 448 buildings of 1266. This concentration can lead to higher prices due to a lack of competition. These large companies might have more negotiating power and could potentially might impose higher fees on condo owners for their services.

- Economies of Scale: Larger companies often benefit from economies of scale, which could allow them to offer services at lower costs. However, if these companies use their size to engage in anti-competitive behaviour, such as hiring their associated service providers and preferable contractors that prevent other companies from entering the market, they could keep condo expenses artificially high.

- Market Influence of Medium-Sized and Big-Sized Companies: The medium-sized companies managing 196 buildings (16%) and big-sized companies managing 391 buildings (31%) have a significant market influence. If these companies follow competitive practices, they could exert downward pressure on condo service prices. Conversely, if they align their pricing strategies with the larger players or face barriers to competition, prices could remain high.

- Limited Impact of Small Companies: Small condo management companies manage 8% of the buildings, indicating a fragmented segment with limited influence on market prices. Given their small market share, they may not be able to significantly impact the overall pricing of condo management services.

- Non-Identified Companies: The presence of non-identified companies managing 10% of the buildings suggests there is some diversity in the market. However, the impact on pricing will depend on how competitive this segment is. This group of building indicated the highest financial efficiency of condo expenses (condo market value per square foot divided by annual condo fee per square foot), and it becomes a breeding ground for a fair competition.

It is obviously that the market dominated by a few large companies might lead to higher costs and less innovation, as there is less incentive to improve services or reduce prices. Conversely, a more balanced market with robust competition among many players could result in more competitive pricing and better service offerings. If there are barriers to entry for smaller or new companies, or if there are practices that prevent competition, then condo owners may face higher prices and have less choice in services.

In summoning a renaissance of competition, the market must embrace a new paradigm—where small and medium enterprises are emboldened to innovate, where condo owners enjoy quality services at just prices, and where the market itself becomes a thriving hub for urban life enhancement.

Related posts:

Top 10 Condo Management Companies that Spend Less Condo Owners' Money to Maintain the Most Expensive...

How to save condo owners' money mitigating the highest risks

What Makes Condo Directors to Select Your Condo Management Company

Are You Thinking about Buying a Rental Property in Toronto?

Surprising Condo Fee Trends during COVID time. Part 2. Condo Age Factor

RED FLAG of critical condominium management risks

Unique numbers and interesting facts blasted maintenance fees' myth

Unveiling the Mysteries Behind Condo Fees in Toronto & GTA: Trends, Anomalies, and Unanswered Qu...

Share via: