Share via:

Directors of Toronto Condominiums initiated “Condo Leaders Group” to unite condominiums and collect reliable numbers to start a petition and request the government’s intervention before the situation becomes a disaster as it did in Alberta and British Columbia, where insurance premiums have increased by 50% to 780% a year, even for a new condominiums with no claims

High premium reaching half a million per year along with exorbitant deductibles reaching $100,000 or more per event have become a reality for condominiums in Toronto.

Some condominium directors initiated Condo Leaders Group to create a group tender in order to obtain competitive insurance rates, deductibles and coverages for condominiums of the group, and protect condo owners’ interests.

If you are a condo director or a condo manager,

your small step might make a difference

to protect your family and families of other condo owners from the experience of condo owners of Alberta and British Columbia.

Just

to be verified and enter your condo insurance data

Insurance Crisis In British Columbia And Alberta

There have been a few sad examples in Alberta of condo owners going into bankruptcy, after condominium accidents related to wildfires of 2017 caused condo insurance to increase by 600%, reaching $925,000 a year for 156 townhomes. And in some cases, it turned out to be impossible for condominiums to renew their insurance, because it was unaffordable for condo owners to pay ~$500 extra per month just for the condominium common element insurance increase.

This year’s spring, BC condo owners were in for a shock when they found out that their insurance was to skyrocket by 780% – particularly Mahogany Tower in Abbotsford faced a steep hike from $66,000 in 2019, to 588,000 in 2020 – and that’s for a claim-free, brand new building. Their premium expenses were a one-time levy of $3,000 per unit, doubling strata fee up to $600 a year for each unit.

A Quick Positive Intervention Of British Columbia Government

In the highly monopolized Canadian insurance market BC have become the first province that has taken the necessary steps to make situation more controllable . A letter from a concerned property owner has prompted legal action by BC condo board members to plead against ever rising insurance premiums and deductibles, and to promote changes to current regulations to address the province’s strata insurance crisis. The provincial government is proceeding with several regulatory changes to address strata insurance market.

Starting November 1st, 2020, insurers are required to provide strata corporations with a 30 days notice if they are not able to renew the insurance, or plan to change their insurance policy.

Will The New legislation In British Columbia Ease The Insurance Crisis?

Housing expert Randy Lippert, author of Condo Conquest: Urban Governance, Law, and Condoization in New York City and Toronto, warned that the rising cost of condominium insurance may soon become unsustainable. “I think there will be a number of condos where those fees become unsustainable, and people will want out,” Lippert told HuffPost Canada.

Those changes might give time and temporary financial opportunities to condo owners, but they might not change the reality of the crisis significantly.

Why Toronto Condo Owners Want To Go Forth

It would be great if Ontario government follows the great example of British Columbia. But the insurance rates might stay the same. The solution to the situation could be figuring out a proper course of actions to protect Toronto condo owners from repeating the situation of Alberta and British Columbia.

Condo owners can all contribute to the highly valuable information of how much their condominiums pay for insurance, how much deductible they have, and how much they have received in accident claims for the past 3 years. This information must be accurate, it should be added by condo directors and/or property managers here:

What Has Been Done By Toronto Condo Directors To Protect Condo Owners?

Condo Directors of Toronto Condominiums initiated “Condo Leaders Group” in November 2020 to organize a group tender to get the best rates of insurance premiums and deductibles for Toronto condominiums. It has been revealed that there are just 2-3 companies on the market that provide insurance for condominiums, and it is next to impossible to get competitive prices for condo owners. And the situation is about the same in many large Canadian cities, which allows us to declare this problem a nationwide problem, rather than just a Toronto problem.

That is why Condo Leaders Group and Condo BI Canada team are concerned about the main reasons behind the steadily growing insurance increase rate of 40 % – 780% a year in Ontario, British Columbia and Alberta.

These are the reasons pointed out by insurance companies, Insurance Bureau of Canada (IBC) and some experts:

Insurance Crisis Reasons Show Interesting Details That May Require Further Investigation

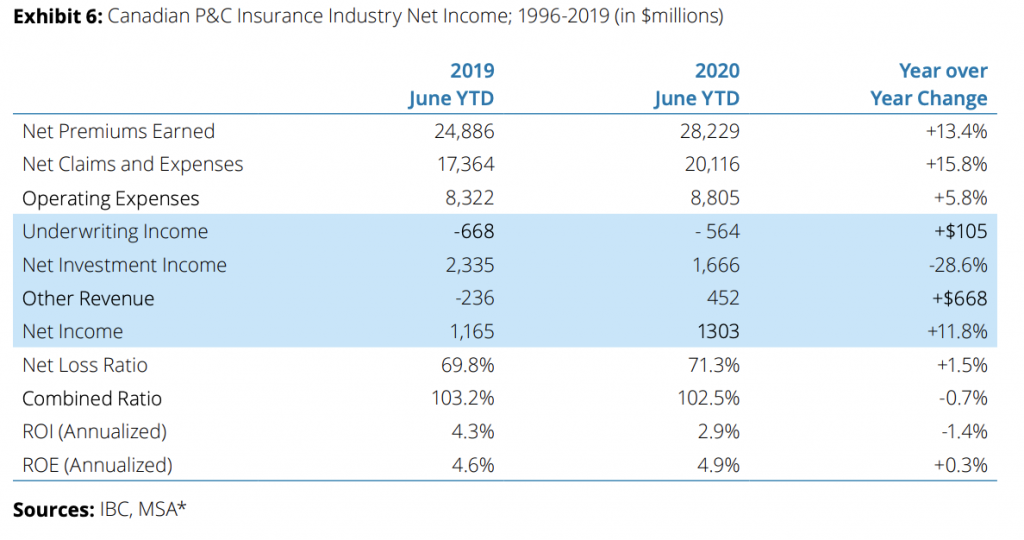

Net Claims and Expenses growth is $573m lower than Net Premium Earned increase in 2020, as per Deloitte’s latest report. It is difficult to assess the number of claims filed by strata and condominium corporations having only publicly accessible information. But based on the latest reputable report Deloitte & Touch State of Canadian Commercial Property & Casualty Insurance Market we can see that “Net Claims and Expenses” annual growth just 2.4 % higher than “Net Premium Earned” (15.8 % – 13.4 %) and “Net Claims and Expenses” increased just by $2,770m while “Net Premium Earned” increased by $3,343m.

Basing on Deloitte’s data it does not seem that insurance companies have a reason to increase the insurance premium and deductible.

It is impossible to distinguish a part of the condo industry data. But it could be a subject for the government audit to identify the course of action needed for the best resolution of the situation

-

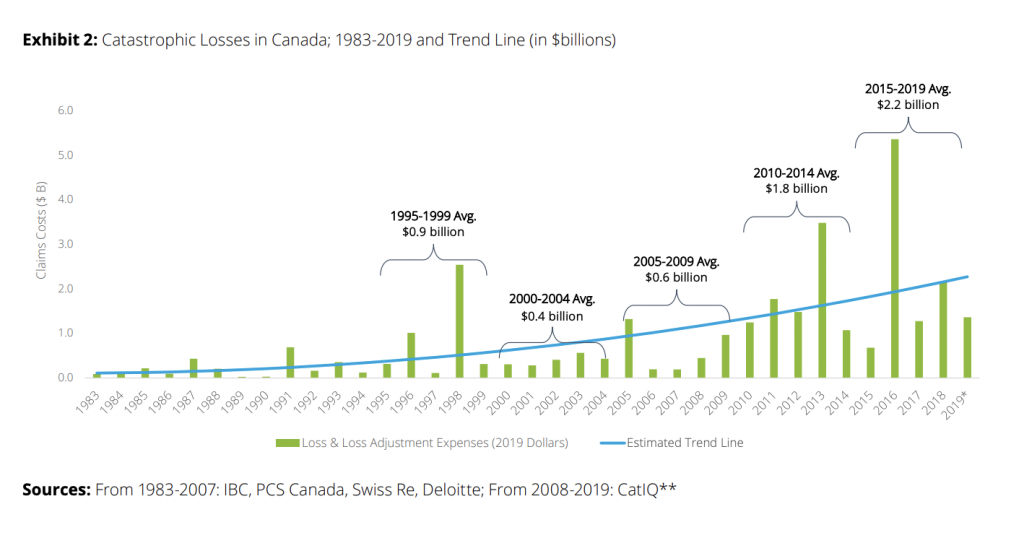

Based on Insurance Bureau of Canada data, In the past 10 years, insured losses due to flooding, wildfires and storms have averaged $1.9 billion a year and $2 billion in 2020

Yes, severe weather might be a reason, but that kind of claims growth is ~ 22.2 % (2.2b -1.8b) comparing to 2010-2014 period, and it is certainly NOT a reason to increase insurance premiums by 40% – 780% a year.

2. It is undisputable that condo management needs risk management improvements, especially in condominiums with high number of claims.

Condo Leaders Group has an intention to investigate how much condominiums pay, how much accidents they have had and how much coverage they received to take appropriate actions.

3. The current economic situation is a very valid reason for insurance companies’ risks growth.

However, commercial property owners having business interruptions and losses caused by the pandemic this year were unable to get compensation for the losses their insurance was supposed to cover.

Yes, it is a hard period for insurance companies, but it is not a reason to transfer this heavy financial responsibility to condo owners’ shoulders.

Inequality Of Rights And Obligations Between Condo Owners And Insurance Companies

It is mandatory for condo owners to get insurance of a condominium’s common element in Ontario. But there is no obligation imposed on insurance companies to ensure all condominiums. And some condominiums cannot get insurance at all. Such situation breaches condo owners’ human rights and creates inequality.

A Possible Alternative to Condominium Insurance

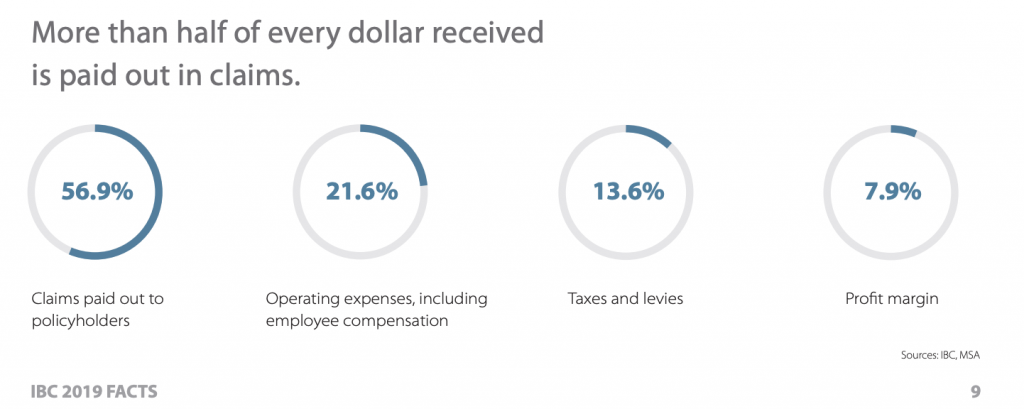

Based on the current situation when Toronto condominiums pay almost $500,000 a year insurance premium and have $100,000 deductible, it would be more reasonable to make a contribution $500,000 a year into some kind of condominium’s own “insurance fund” that could be corrected from year to year based on accidents history, and in case of an accident to pay for everything by itself rather than paying $500,000 -$900,000 to the insurance company every year. It could save condo owners about 43 % on average, because according to a report of Insurance Bureau of Canada (page 9), there is ~ 57% of revenue paid out to policyholders and ~ 43% insurance companies’ expenses, taxes, and profit margin:

The requirements of the Competition Act, August 2003 must be provided

by the government

Finally, taking into account that condominium insurance rates in Toronto become uncontrollable and that market is almost monopolized in Toronto, Ontario and other Canadian Provinces, it would be fair if condo owners requested the government intervention to regulate the situation with condominium insurance and enforce compliance with the federal law Competition Act of August 2003 that requires to “provide consumers with competitive prices and product choices” and “prevent anti-competitive practices in the marketplace that is breached in condo insurance market”.

If you are a condo director and/or a property manager, and wish to make condo insurance situation transparent for condo owners, the government and the insurance companies, please make a small step to protect yourself:

to request our provincial government to take proper actions on condo insurance and protect condo owners!

Little drops of water make a mighty ocean! We have great power if we are together!

Related posts:

Sell Your Condo Unit without any Comission!

Self-Managed vs Professionally-Managed Condominiums. 98 % of Toronto & GTA's Condos Could Spend...

What do condo owners not know about Property Management Company’s service price?

How Much Does Bullying of Condo Directors Cost to Condo Owners

Surprising Condo Fee Trends during COVID time. Part 2. Condo Age Factor

Surprising Condo Fees Trends during COVID time

Initiating "Condo Leaders' Group" for Open Fair Tender to Get the Best Terms for Condominiums' Insur...

6 % Condominiums of Toronto & GTA Decreased Condo Fees during COVID time

Share via: